As the United States prepares to celebrate its 250th birthday, we thought it would be interesting to take a peek at what "financial independence" looked like in 1776. Because, in many ways, the financial world of 1776 would be almost unrecognizable today.

In those early days, around the time of the Revolutionary War and the signing of the Declaration of Independence, Americans didn’t have checking accounts, mortgages, or retirement plans. We didn’t even have a national currency. There were no ATMs, mobile banking apps, credit scores, or online payment systems.

And yet, despite all those differences, many of the financial goals associated with the “American Dream” were remarkably similar to those we have now: supporting a family, preparing for the unexpected, and creating opportunities for future generations.

Money Was Complicated

Today, most Americans carry American currency in their wallets and can make purchases with a tap of a card or phone. Two hundred and fifty years ago, things were far less straightforward.

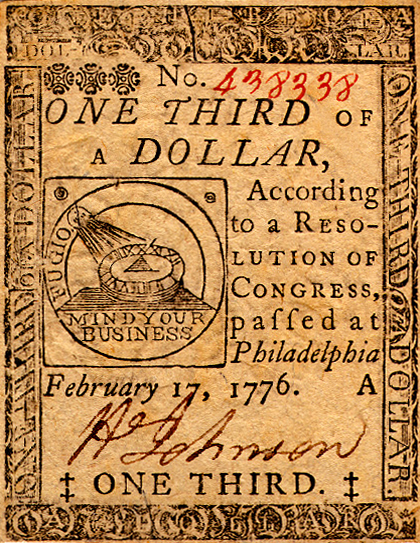

Before the Coinage Act of 1792—which established the U.S. dollar as the standard, created the U.S. Mint, and introduced the decimal system—colonists used a mix of European and South American currencies, Spanish dollars, Continentals, and other forms of money. Some of the most common were:

- Spanish dollars ("pieces of eight") - Minted from silver mined in the Americas, Spanish dollars became one of the most widely accepted and trusted currencies in the colonies. They were commonly called "pieces of eight" because the coins could be physically cut into eight wedge-shaped pieces, allowing people to make smaller purchases when exact change wasn't available.

- British pounds, German thalers, and other foreign coins - Colonial Americans regularly used a mix of foreign coins and currencies, especially in areas involved in international trade. But the value of these currencies varied from colony to colony.

- Continentals (see left) – Paper money issued by the Continental Congress during the Revolutionary War. Unfortunately, overprinting and inflation caused the currency to lose much of its value, giving rise to the phrase “not worth a Continental.”

Across the colonies, coins were often in short supply, especially in rural communities. So, in some regions, colonists relied on locally issued paper currency, handwritten ledgers, and even commodities such as tobacco when coins were scarce. The result was a confusing financial system in which multiple currencies circulated simultaneously and exchange rates were not always consistent from one colony to another.

Banking Was Rare

In 1776, modern banking was still in its infancy. In fact, the first federally chartered U.S. bank wouldn’t be established until 1791. American credit unions were even farther in the future, with the first U.S. credit union not opening until 1908—more than 130 years after the Declaration of Independence was signed.

For colonists in the 1700s, banking was simply not a routine part of life, and most Americans went their entire lives without ever opening a bank account. Back then, banks were few in number, concentrated in major cities, and largely focused on financing trade and commerce. Even where banks existed, they primarily served merchants, governments, and wealthy individuals involved in trade.

Credit Looked A Lot Different

Without local banks on every corner, people often stored cash at home. When they needed to make larger purchases, they relied on personal relationships for loans or worked directly with merchants who extended credit. Trust and reputation played a major role in the economy, and a person's financial decisions could affect their standing in the community for years-or even generations.

Because coins were often scarce, many colonists relied on book credit to purchase goods such as flour, tobacco, coffee, housewares, fabric, and tools. These purchases were recorded in handwritten ledgers, and customers would pay later, sometimes weeks or months after the transaction occurred.

Farmers, for example, frequently purchased supplies on credit with the expectation that they would repay the debt after selling crops or livestock later in the season. Credit arrangements often involved goods rather than cash, so a customer might repay their debt with crops, livestock, labor, or other commodities.

There were no credit scores or formal credit reports. Instead, merchants often decided whether to extend credit based on a person's reputation, relationships, and history of repaying debts within the community. A customer who failed to repay a debt could find it much more difficult to obtain goods or credit in the future-and in close-knit communities, that reputation could affect opportunities for family members as well.

In severe cases, unpaid debts could also lead to imprisonment. Debtors' prisons existed in colonial America and remained legal in parts of the United States well into the nineteenth century.

Retirement Wasn’t Really a Thing

For many Americans, retirement as we know it simply didn't exist in the 1770s. Although life expectancy at birth was relatively low at the time, it was not unusual for adults who survived childhood to reach their 60s or 70s. Few colonists, however, had the option to stop working entirely. Farmers continued to tend their land, tradespeople continued their craft, and family businesses were often passed from one generation to the next. Most colonists worked as long as they were physically able.

Social Security would not arrive until 1935. Before then, America’s closest equivalent to a national retirement program was a series of military pension systems. In fact, the Continental Congress approved pensions for disabled soldiers in 1776, and later generations of veterans would receive benefits through expanding federal pension programs. However, these benefits were generally limited to veterans and their families rather than the population as a whole.

The ultra-wealthy-including plantation owners, merchants, and aristocrats-often passed their estates to their heirs while continuing to collect income from land or investments. For everyone else, aging frequently meant relying on family members, community support, or continued employment.

Without pension plans, 401(k)s, or Social Security, the outlook was often grim for those who lacked savings or an inheritance. Many relied on local parishes, municipal relief, or were forced into almshouses (poorhouses), where residents typically lived and worked in exchange for basic support.

Homeownership Meant Something Different

Homeownership—often considered a cornerstone of the American Dream—looked different in 1776, but it represented many of the same ideals it does today: opportunity, stability, and independence.

There were no 30-year fixed-rate mortgages or standardized lending requirements. Instead, land purchases were often financed through private agreements between buyers and sellers, loans from wealthy individuals, or family connections. In some cases, buyers paid for property in installments over many years.

Property ownership also carried greater significance than it does today. In many colonies, owning a certain amount of land was a requirement for voting or holding public office, making it both an economic asset and a source of political power.

Property ownership was also not equally accessible to everyone. Women, enslaved people, and many others faced significant legal and social barriers to acquiring or controlling property. And, while some unmarried women could own property and conduct business, married women generally had few independent property rights. Under the legal doctrine of coverture, a married woman’s finances and assets were often controlled by her husband. In many colonies, widows had more financial independence than married women, because they could inherit property and manage estates in their own names. Even so, legal and social barriers often made it more difficult for women to conduct business, protect property rights, and participate fully in public life.

For those who could afford it, land ownership was often the closest thing to a retirement account, investment portfolio, or family legacy. Farms, homes, and businesses were typically passed down through generations, helping families build wealth long before modern financial markets became widely accessible.

In many ways, property served multiple purposes at once: a place to live, a source of income, and a means of building and preserving wealth for future generations.

Some Things Haven’t Changed

To get through difficult times in 2026, we often turn to insurance policies, emergency savings accounts, or government programs. And when those resources fall short, many of us still rely on family, friends, neighbors, and community organizations for support.

In 1776, when government aid and insurance options were limited or nonexistent, people also relied on families, churches, neighbors, and local organizations to get through hardships. Whether it was sharing resources after a poor harvest or helping a family rebuild after a disaster, community and mutual support were often essential.

And frankly, the idea that people could accomplish more by working together has remained an important part of American life ever since. Over time, that spirit of cooperation inspired everything from mutual aid societies and community organizations to the Credit Union Movement itself.

While the tools we use to manage money have changed dramatically over the last 250 years, the underlying goals are surprisingly familiar.

We still want financial security, but we also want to build better futures for ourselves and those we care about.

That's the kind of freedom people were pursuing in 1776, and it's the kind of freedom many of us are still working toward today. Because at its core, financial freedom has never been just about money. It's about having the ability to make choices, weather challenges, and invest in what matters most.

Want to learn more about the history of money and banking?

- Discover the history of credit unions in Oregon and beyond.

- Learn the history of Maps Credit Union.

- Explore the history and evolution of money.

- Read about the history of piggy banks.